"I want high Sharpe ratios. If a manager does not have a high Sharpe, forget about it, I'm not interested. He is cut from my list. We only invest in high Sharpe managers."

You have all heard or may have used those phrases. This is based on the simple view, "If I invest in a set of high Sharpe ratios, I will have a portfolio that has the highest Sharpe ratio possible". Not exactly. I can actually increase portfolio Sharpe by adding uncorrelated investments even if these Sharpe ratios are lower than the existing portfolio. These second order effects of diversification are meaningful.

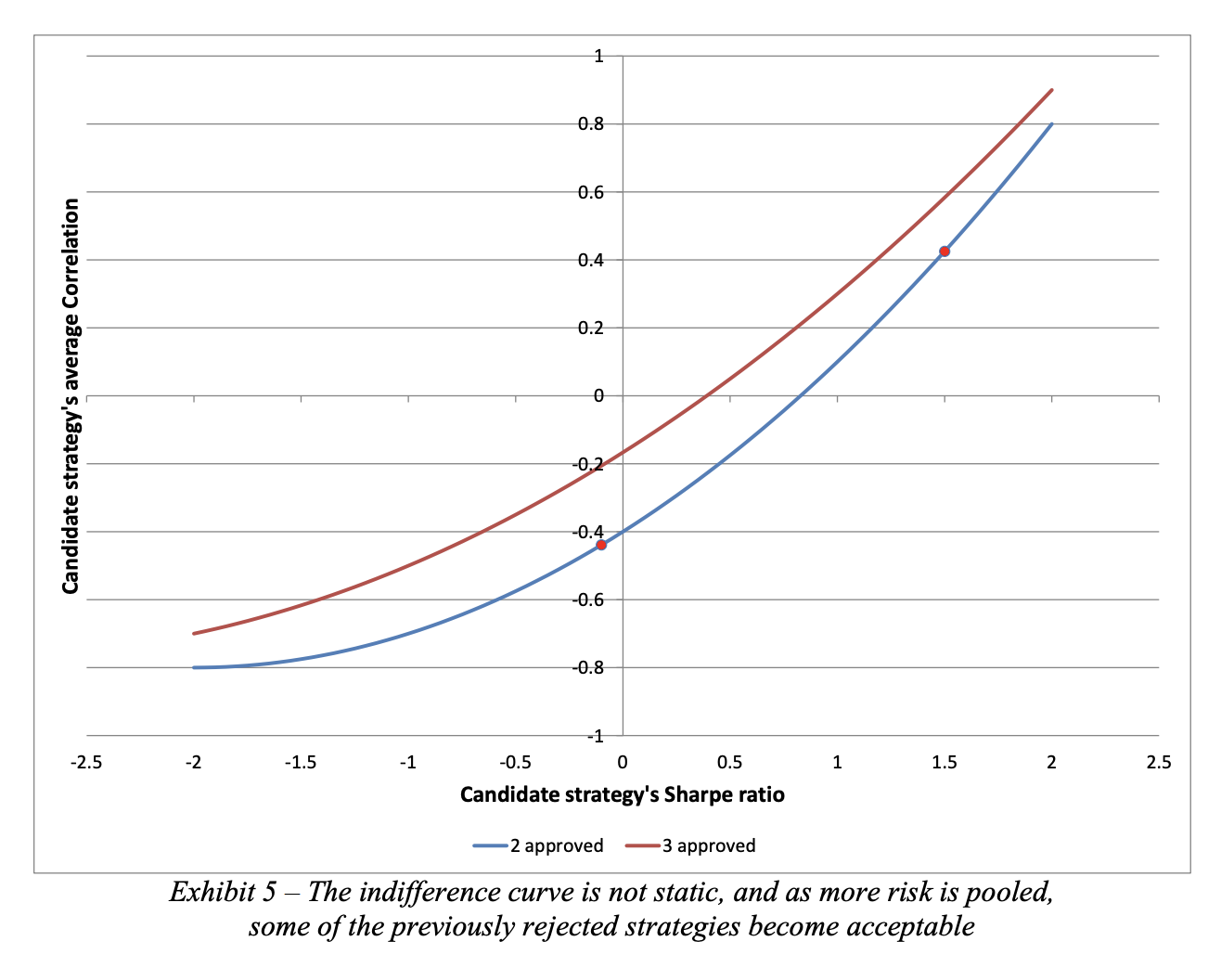

An approved set of strategies can be indifferent between a new investment's Sharpe ratio and its average correlation to a portfolio. The impact of adding a high Sharpe ratio with a high average correlation can be the same as a lower Sharpe and lower correlation investment. This can be a hard concept to accept. It is an even harder concept to implement. How easy is it to go to an investment committee and say, "I know this manager is not as good as others, but he is a great diversifier"? The answer will likely be, "That is great, but I don't eat diversification". Nevertheless, the simple math in the paper, "The strategy approval decision: A Sharpe ratio indifference curve approach"

The blend, not the individual Sharpe ratio, is the critical issue with adding a new strategy investment. The paper provides some useful graphs which help to describe the dynamics between Sharpe ratios and correlation. The improvement of the portfolio Sharpe ratio is non-linear with respect to falling correlation. More strategies will improve the portfolio Sharpe for any given correlation, but greater improvement will come when correlations are low. This is consistent with the fundamental law of active management, add trades that are uncorrelated.

There is a trade-off between Sharpe and correlation that is measurable. Investors can find a lower Sharpe strategy that will have the same value as a higher Sharpe ratio based on its correlation. This why finding different strategies to include in a portfolio mix is so important.

There is a trade-off between Sharpe and correlation that is measurable. Investors can find a lower Sharpe strategy that will have the same value as a higher Sharpe ratio based on its correlation. This why finding different strategies to include in a portfolio mix is so important.

Every hedge fund investor should have the idea of a Sharpe ratio versus correlation indifference curve emblazed in his mind. It is not a hard concept but is not at the forefront of the strategy approval process.

Every hedge fund investor should have the idea of a Sharpe ratio versus correlation indifference curve emblazed in his mind. It is not a hard concept but is not at the forefront of the strategy approval process.

The blend, not the individual Sharpe ratio, is the critical issue with adding a new strategy investment. The paper provides some useful graphs which help to describe the dynamics between Sharpe ratios and correlation. The improvement of the portfolio Sharpe ratio is non-linear with respect to falling correlation. More strategies will improve the portfolio Sharpe for any given correlation, but greater improvement will come when correlations are low. This is consistent with the fundamental law of active management, add trades that are uncorrelated.

No comments:

Post a Comment