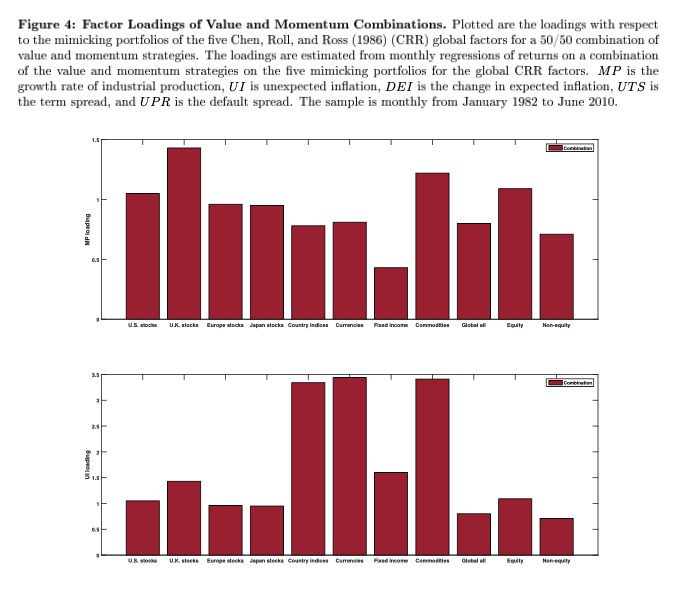

The paper, "A Global Macroeconomic Risk Model for Value, Momentum, and Other Asset Classes" looks at why value and momentum is an good combination of alternative risk premiums as a portfolio from the perspective of sensitivity to macro factors. Past work has shown that value and momentum complement each other given their low correlation, but there has not been a good rationale for this combination. The authors in this paper try to look at different macro factor loading to answer this question.

For their macro factors, they use the Chen, Roll, and Ross (CRR) macroeconomic risk factors. The CRR factors are a well-defined set which includes the term premium, default premium, industrial production, expected inflation, and unexpected inflation.

The negative correlation between value and momentum is caused by the different sensitivities to macro factors. Value has a strong positive load to the term spread but negative factor loading on all the other macro features. In the case of momentum, there is a negative close to zero loading on the term premium, but there are strong positive loading on the other four macro factors, growth in industrial production, unexpected inflation, change in expected inflation and the default spread. Nevertheless, because the factor loadings are different, it is not the case that forming an equal weighted portfolio between value and momentum will lead to a portfolio that is market neutral to macro factor loadings. Changing the weights will give an investor a tilt to the loadings desired.