Campbell's Law - The more any quantitative social indicator is used for social decision-making, the more subject it will be to corruption pressures and the more apt it will be to distort and corrupt the social processes it is intended to monitor

Jerry Muller's corollary to Campbell's Law, "Anything that can be measured and rewarded will be gamed."

Goodhart's Law, "Any measure used for control is unreliable." or "When a measure becomes a target, it ceases to be a good measure."

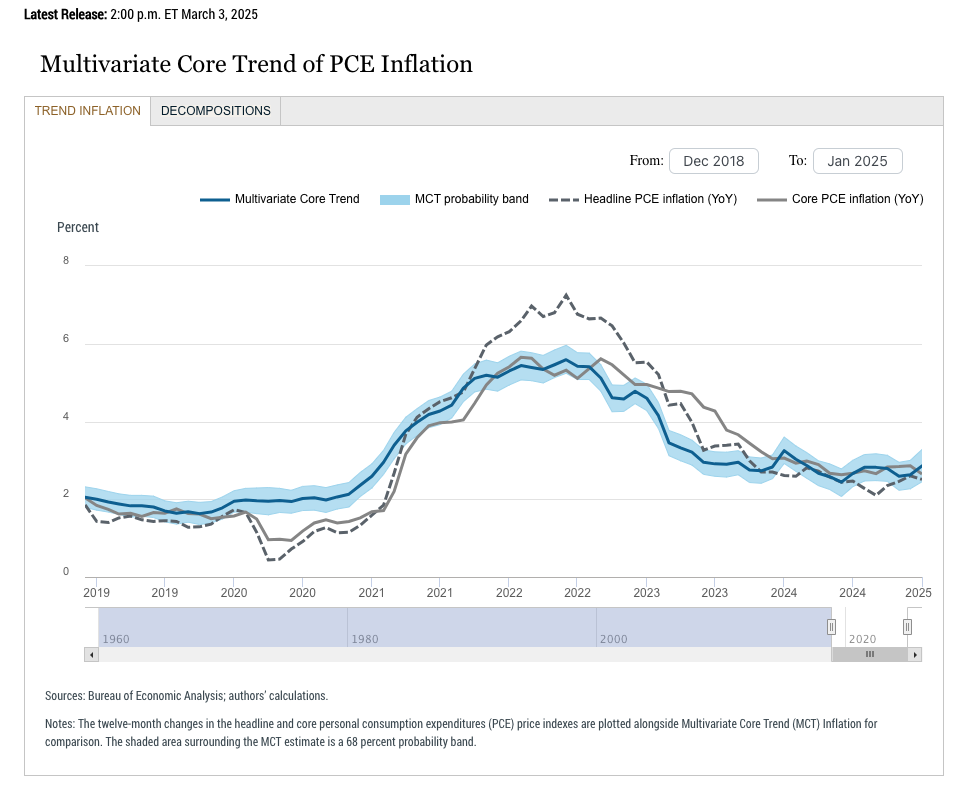

Let's think about the 2% inflation target. Why do we need to have a 2% target? What makes it so special? How close do we have to get to 2% to say the Fed is successful? What happened to an average inflation rate of 2%? If we want to average to a 2%, then should the Fed push to something below 2%?

Can you have deflation and economic growth? Is there something like good deflation and bad deflation?

It is becoming increasingly clear that the focus on some arbitrary target can lead to more economic problem. If we control price inflation, we may just allow for greater asset price inflation. The goal is not some inflation number but stable purchasing power and effective growth. This may mean that the Fed intervenes in markets to provide financial stability but that is a last resort and not a policy of denying loses. We should not be data driven but goal driven. Let's be clear on the goals and why they are relevant.