Investors have measured partial correlation to look at the risk impact when markets decline. They have used the term crisis alpha to describe the change in downside correlation for styles like trend-following. These statistics are all descriptions of what investors really want - convexity. The bending of beta under different regimes or market behavior is critical to successful diversification and portfolio performance, so investors should study style convexity.

My friend Artur Sepp of QuanticaCapital AG has done some interesting work on this topic. He presents some of his research results in a speech, "Convexity of Trend-Following Strategies" at the QuantMinds conference, May 2019. He does a good job of showing the relative value of trend-following versus other hedge fund strategies. It is the only strategy that shows positive beta in up markets and negative beta in down markets.

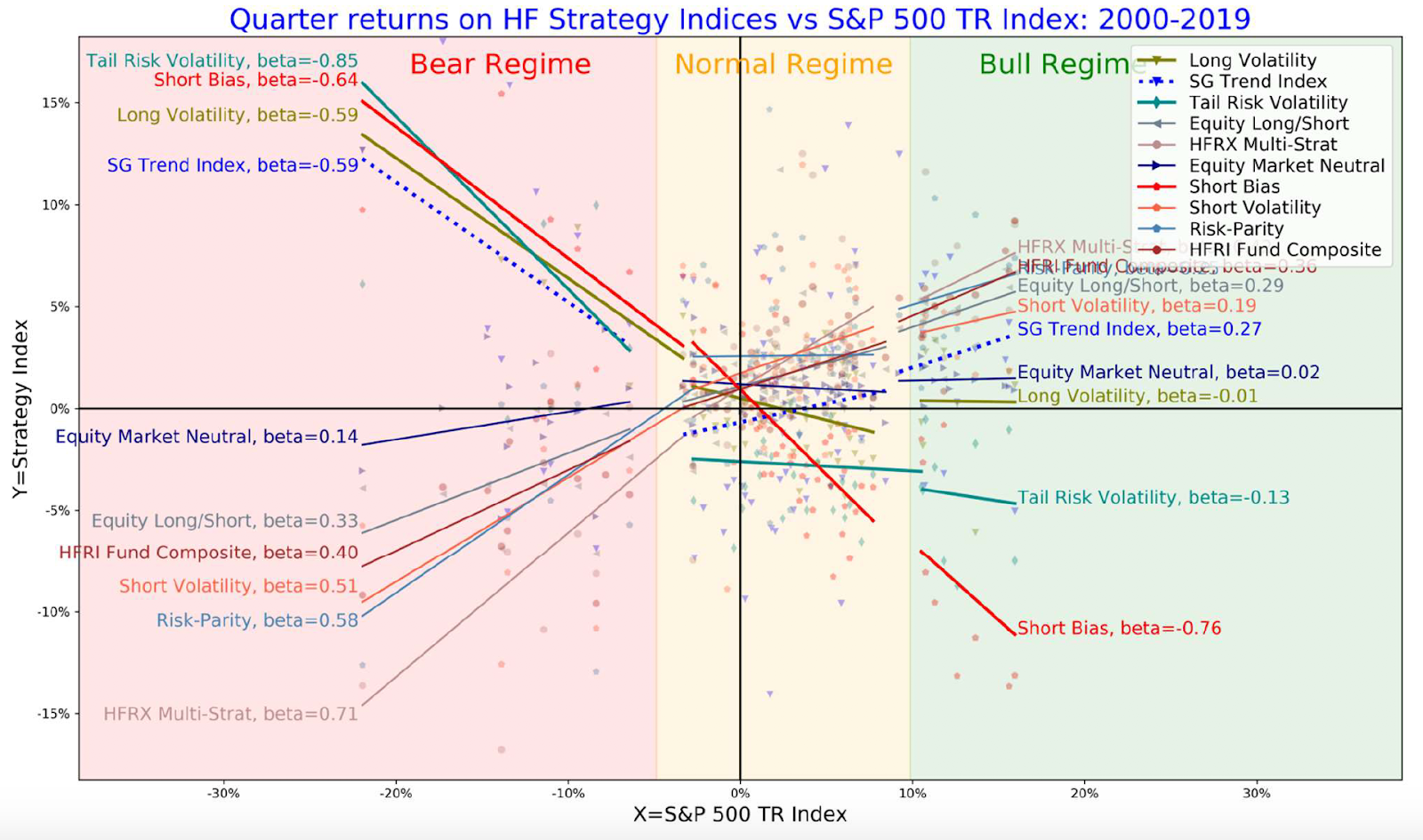

Sepp breaks-up equity markets into three regimes, bear, normal, and bull and uses conditional regression to measure differences in beta. He finds that there is strong convexity for some strategies and not for others. This convexity appears when we looker over longer holding periods like a quarter. However, there is a cost with buying convexity in that Sharpe ratios are lower for those strategies that exhibit this behavior. Or, those strategies that have higher beta in bear markets need compensation in the form of higher Sharpe ratios. Convex strategies also are related to return skew. Higher Sharpe ratios are associated with negative skew.

Partial correlations and conditional betas are not hard to measure and add an important dimension to portfolio construction. These concepts have been known for some time, but conducting an analysis across the set of hedge fund styles adds context to this discussion and truly shows the trade-offs with investment choices. The positive convexity feature of trend-following does not change the fact that performance over the last few years has been difficult for this strategy; nevertheless, it is important to know key return dynamics.

No comments:

Post a Comment