Alternative risk premia or cross-sectional factor strategies generally have low correlations with equity and bond market betas, but that it not the same thing as no market beta exposure. Market betas will differ by strategy and will also change with the market environment. A portfolio of ARP strategies will have implicit beta exposure and investors need to account for these risks when constructing a portfolio.

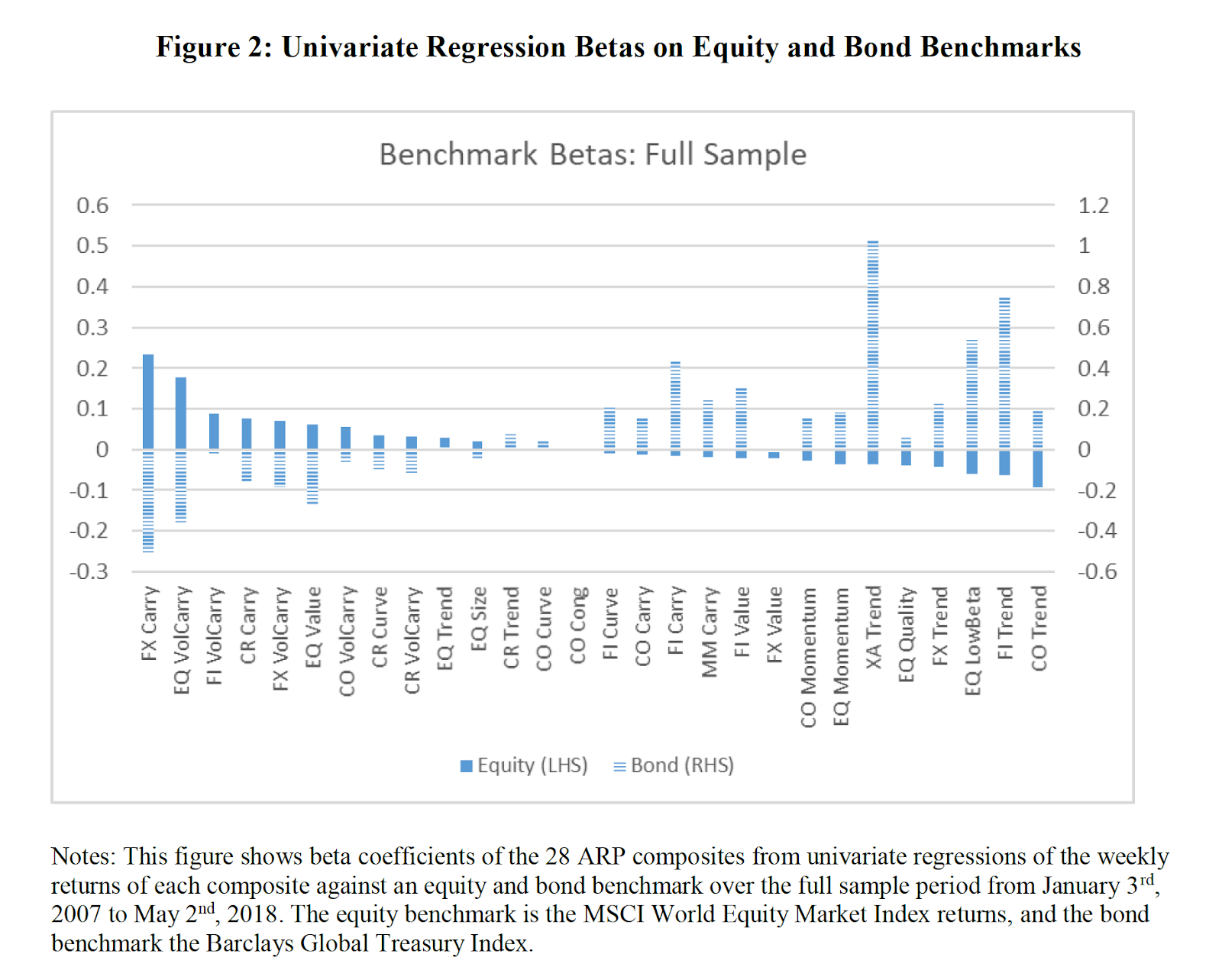

Using tables and figures from the paper "A Framework for Risk Premia Investing: Anywhere to Hide" by Kari Vatanen and Antti Suhonen, we can see that there are ARP strategies that are equity beta sensitive and bond sensitive. The simplest breakdown is that carry strategies have, on average, more equity beta exposure while momentum, trend, and value are more bond sensitive. If you are looking for defensive strategies focus on momentum and trend. Carry may have low equity beta but will still be more sensitive to a risky asset move. This is one of the clear reasons why carry and trend provide good diversification benefit when combined in a portfolio.

These alternative risk premia strategies will also be affected differently by "good" and "bad" times. The beta in up markets may not be the same as the beta in down markets as seen in the table below which compares betas in different quintiles.

The differences in betas can be visually displayed in a graph between betas for the lowest quintiles versus all other quintiles. A difference away from the straight line tells us the amount of beta variation risk. This dispersion is what will surprise investors who expect protection from low beta and don't get it when needed for some strategies or get more diversification than expected with other strategies. Data below the line states that estimated beta in the lowest quantile is lower than the other quantiles. Those above the line suggest greater beta risk.

No comments:

Post a Comment