Risk premia across assets have been extensively tested but over different time periods and using different testing methodologies. Risk premia have existed for as long as we have data across a wide set of asset classes and for a number of different styles including value, momentum, carry and defensive. The value of risk premia is well documented by the research folks from AQR Capital in their opus "Factor Premia and Factor Timing: A Century of Evidence" that was updated last month. This research piece provides a wealth of information and thoroughness which should make this paper required reading for those who want to get a full analysis of the historical numbers associated with risk premia. I will break up a summary of their work into two parts, the performance measurement of risk premia, and the potential timing of the risk premia.

The broad risk premia tested have real economic value that has stretched back for long time periods. This research extends the measure of risk premia to almost a century of data confirming what other researchers have found, but in a number of novel ways. Unfortunately, in our next post we will summarize their work on timing which suggests that after testing a wide battery of alternative models, profits from conditional forecasts is unlikely.

Foremost with this work, the returns from risk premia are real. They are significant for core styles like value, momentum, carry, and defensive. They are present for equities, rates, commodities, and currencies as well as US and international stocks. The value-added is all the more significant when bundled across asset classes or styles.

However, a careful look at the data suggest that excitement about the value-added for risk premia investing should be tempered through comparing the data before and after the original sample used for finding these premia. Generally, the original data sets show stronger results. Thus, it is fair to conclude that risk premia are meaningful but not as significant as found in initial research. The value of risk premia is sample and test dependent. At a minimum, there is clear time variation with risk premia. At worst, some of the results present are from data-mining.

However, a careful look at the data suggest that excitement about the value-added for risk premia investing should be tempered through comparing the data before and after the original sample used for finding these premia. Generally, the original data sets show stronger results. Thus, it is fair to conclude that risk premia are meaningful but not as significant as found in initial research. The value of risk premia is sample and test dependent. At a minimum, there is clear time variation with risk premia. At worst, some of the results present are from data-mining.

The rationale for the time variation of risk premia is not clear. An extensive set of factor for contemporaneous and predictive economic news shows mixed explanatory results. There are only a few macro factors that have meaningful impact on returns. More work on these relationships should be conducted. While this is disappointing, it not overly surprising given the generally poor link between macro variables and market returns.

The rationale for the time variation of risk premia is not clear. An extensive set of factor for contemporaneous and predictive economic news shows mixed explanatory results. There are only a few macro factors that have meaningful impact on returns. More work on these relationships should be conducted. While this is disappointing, it not overly surprising given the generally poor link between macro variables and market returns.

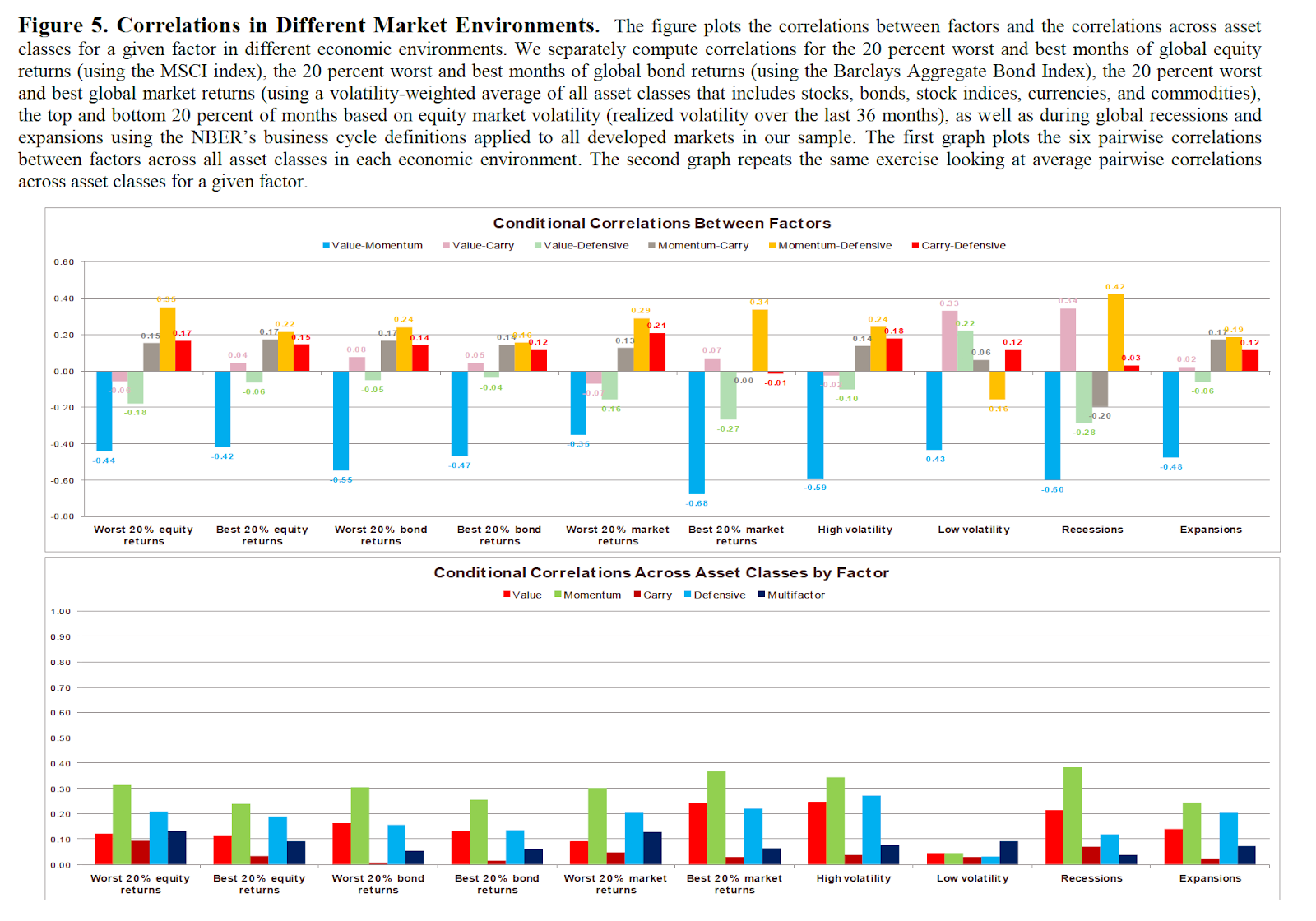

It is also found that the correlations between the market portfolio and risk premia are also time varying and fit within a wide range. Still, the data show some relationships, such as the negative correlation between value and momentum are quite strong regardless of the market environment. These relationships help to form the basis for any portfolio construction of risk premia.

The extensive research on risk premia draws some simple conclusions:

The extensive research on risk premia draws some simple conclusions:

Foremost with this work, the returns from risk premia are real. They are significant for core styles like value, momentum, carry, and defensive. They are present for equities, rates, commodities, and currencies as well as US and international stocks. The value-added is all the more significant when bundled across asset classes or styles.

One of the key benefits of these core risk premia is that they have low correlation. They are generally unique, yet the correlations between them are highly variable. The correlation calculated today cannot be expected to remain the same. A portfolio of risk premia will have highly variable performance and risk characteristics. Nevertheless, the data show that some pairing of risk premia like value and momentum will consistently show negative correlation.

It is also found that the correlations between the market portfolio and risk premia are also time varying and fit within a wide range. Still, the data show some relationships, such as the negative correlation between value and momentum are quite strong regardless of the market environment. These relationships help to form the basis for any portfolio construction of risk premia.

- Risk premia are significant across a wide set of styles and asset classes.

- However, identified risk premia are subject data-mining of the original testing period and the long history suggests are more tempered view on return.

- Correlations across styles, asset class are time varying. The correlations with the market portfolio are also variable.

- There are some significant economic factors related to risk premia, but there is no strong consistent pattern across style and asset classes.

- There are some consistent patterns of correlation among risk premia for different market environments.

No comments:

Post a Comment