All the buzz this summer has been about the strong surge in retail investor activity. Some have argued that the combination of being shut-in, excess savings from stimulus, and the constraints on discretionary spending are the leading cause for retail stock trading. Another plausible explanation could be the increase in investor confidence that a crash will not occur.

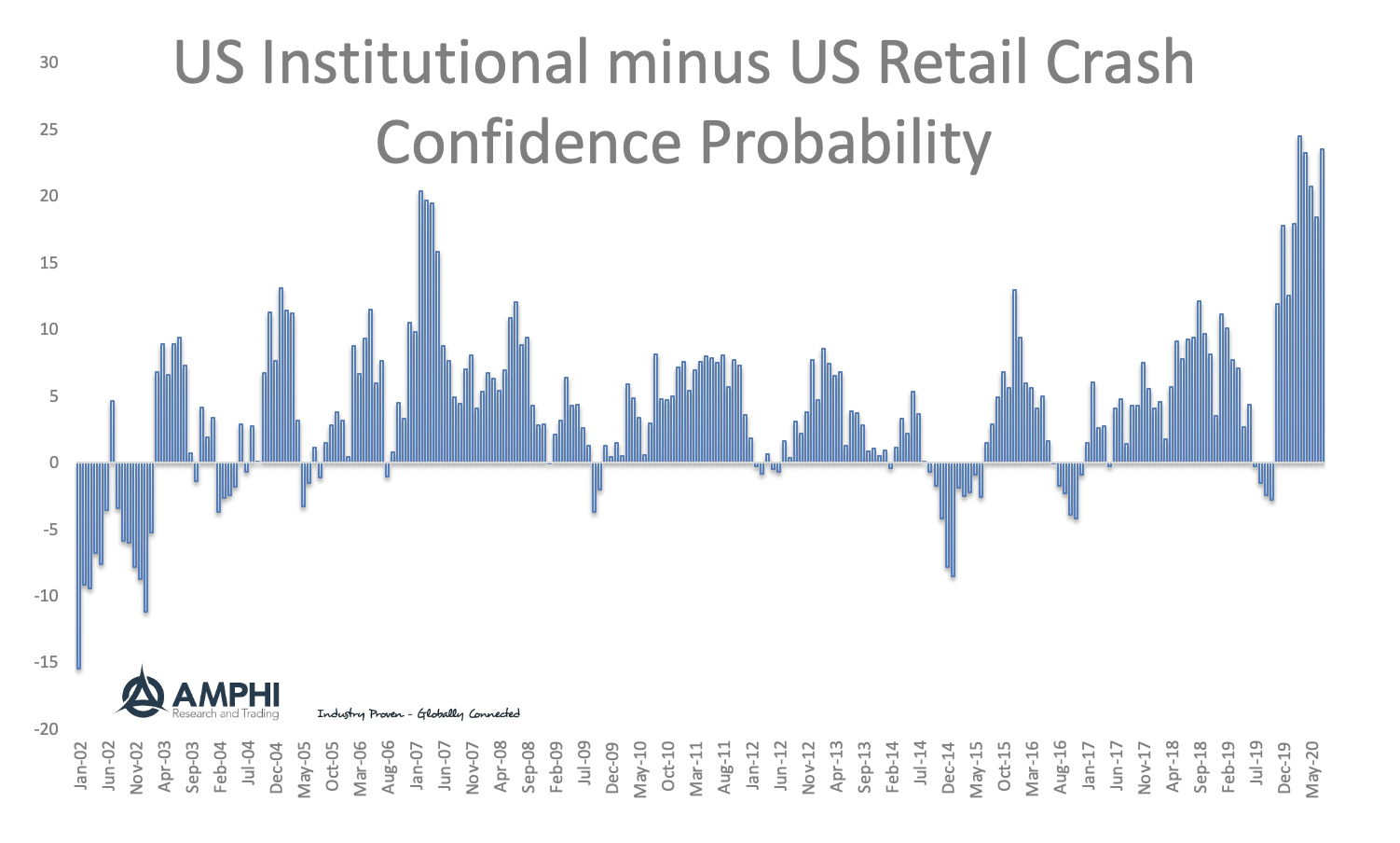

Using survey data from the International Center for Finance at Yale University, we track a subjective measure of crash confidence for close to twenty years. The survey asks a simple question about the probability of a market crash like 1987. See below. Of course, this is not the same as asking whether there will be a sustained bear market or whether an investor is confident about further increases in equity prices, but it provides some useful insight. Institutional respondents currently say there is a higher likelihood of a crash at 40% versus 17% for retail investors. This is a wide gap and has been the widest period in the monthly history. No crash, no risk, buy stocks.

Using survey data from the International Center for Finance at Yale University, we track a subjective measure of crash confidence for close to twenty years. The survey asks a simple question about the probability of a market crash like 1987. See below. Of course, this is not the same as asking whether there will be a sustained bear market or whether an investor is confident about further increases in equity prices, but it provides some useful insight. Institutional respondents currently say there is a higher likelihood of a crash at 40% versus 17% for retail investors. This is a wide gap and has been the widest period in the monthly history. No crash, no risk, buy stocks.

What do you think is the probability of a catastrophic stock market crash in the U. S., like that of October 28, 1929 or October 19, 1987, in the next six months, including the case that a crash occurred in the other countries and spreads to the U. S.? (An answer of 0% means that it cannot happen, an answer of 100% means it is sure to happen.) [Fill in one number]

Surprisingly, in another survey question, US institutions are more confident that the market will move higher over the next year than US retail customers which conflicts with the evidence on crash risk. US retail are less confident about the potential upside for stocks but believe that there is a less chance for a crash. Untangling investor behavior is never easy, but this is suggestive of the strong retail to institutional interest in stocks.

This still does not address why retail investors are so optimistic. They seem to have internalized the Fed's financial protection policy. Current Fed behavior is not like the old Greenspan put but a core policy to provide liquidity and stability if market downside risks appear.

This still does not address why retail investors are so optimistic. They seem to have internalized the Fed's financial protection policy. Current Fed behavior is not like the old Greenspan put but a core policy to provide liquidity and stability if market downside risks appear.

No comments:

Post a Comment