We are faced with an uncertain environment where we don't know whether this is just a bear market that will be corrected, or whether we are headed for a real economic disaster and major market selloff. Some will argue we are already there.

There can be a good story for each, but since these scenarios having changing probabilities the pricing of these disasters only unfolds over time. We often do not know whether we are facing a Great Depression or a Great Recession. Mild or severe, a future disaster is not clear given that the market faces imperfect information. Ex post, the signs may seem obvious, but not ex ante when information is unclear and strong beliefs are hard to form.

The result is that equity prices will only gradually react to consumption declines as investors learn, uncertainty is resolved, and imperfect information is clarified. See "Learning, Slowly Unfolding Disasters, and Asset Prices". I will not go through all the specifics of the model but point out the key point that when there is imperfect information and learning about a large potential disaster, the price asset price paths will often be slow to discount these big moves.

In this type of environment, the world is not efficient in the traditional sense but subject to trends as risk is repriced through time. The slow revealing of information and learning means that deep out of the money downside put protection may not serve investors well because the gradual adjustment does not allow the full put value to be realized. It also means that the VIX, and variance risk premia will only slowly adjust to a pending disaster. Consumption will be affected differently if market prices slowly adjust, a slow grind of a negative wealth effect.

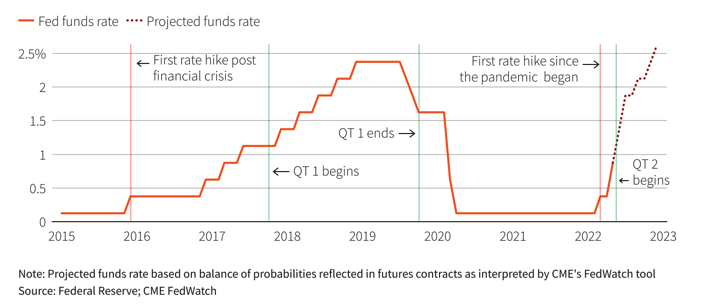

The dynamic of this model fit well with the current environment. I am not suggesting a disaster, but a soft or hard landing, overshooting of policy, or a changing inflation environment is only being revealed slowly and prices are reacting in a similar fashion.

{kind=link}