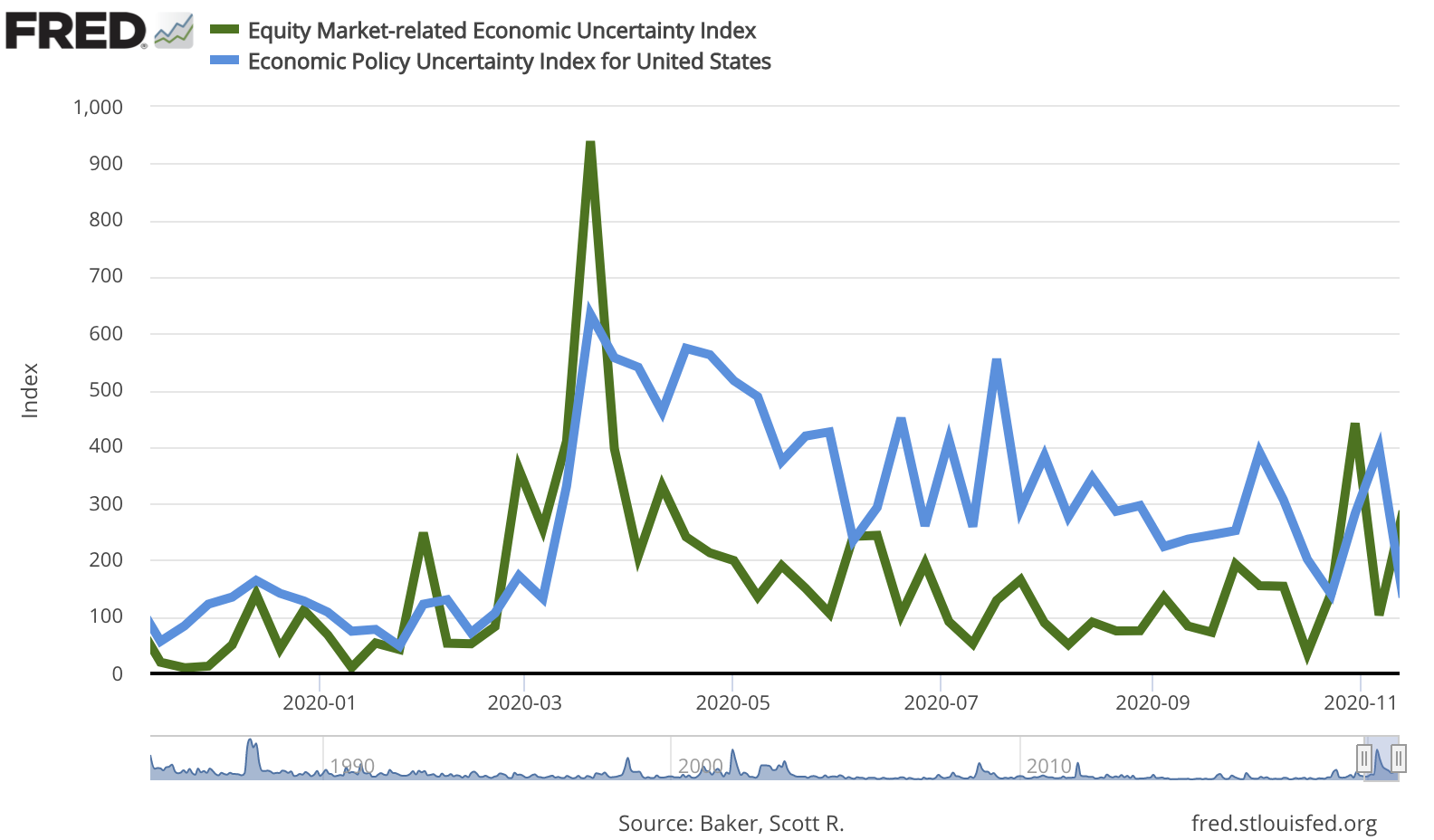

The US inflation story has been a mash-up of different ideas. Go back two years and we were seeing Fed rate increases because of inflation concerns and a desire for normalization; four in 2018 and 9 since December 2015. 2019 saw rate cuts in an effort to support the economy and inflation. March 2020 caused the Fed to pull out all of the stops with monetary policy to push inflation above target given fears of recession and deflation.

The deflation threat has not materialized. The PCE has stayed above 2015 levels and never moved negative. CPI fell dramatically but has bounced back. The lockdown price behavior has not acted like a normal recession.

Inflation numbers will be affected by many relative price shocks and will have a fair amount of noise, so a number of Fed banks have developed smoothed inflation series.

- Dallas Fed - Trimmed mean PCE

- Cleveland Fed - Median and trimmed-mean CPI

- Atlanta Fed - Sticky-price CPI

- New York Fed - Underlying Inflation Gauge

The average of the smooth series shows inflation above 2%. The smooth trends are slightly downward but not suggestive of a deflation problem.

- Dallas Fed - trimmed PCE 1.7%

- Cleveland Fed - median CPI 2.5%

- Atlanta Fed Sticky-price 2.0%

- New York Fed prices-only UIG 2.1%

Did the Fed save the US from a deflation debacle through strong money growth or was the deflation threat never a real problem? We may need more information to provide an answer, but a vaccine that opens the economy will also prime inflation to move higher from a 2% base.