I’ve never heard such a chorus of repeated phrases such as “fixed income replacement” and the “new 40.” - John Bowman CAIA comments at Miami hedge fund conferences

The drumbeat continues for changes in the 40% of the classic 60/40 stock/bond mix. Dump the fixed income and get some alternative investments. This alternative theme has been around for years but has increased in intensity - don't think of hedge funds as high-performance strategies but as substitutes for the low performance bond portion of an asset allocation.

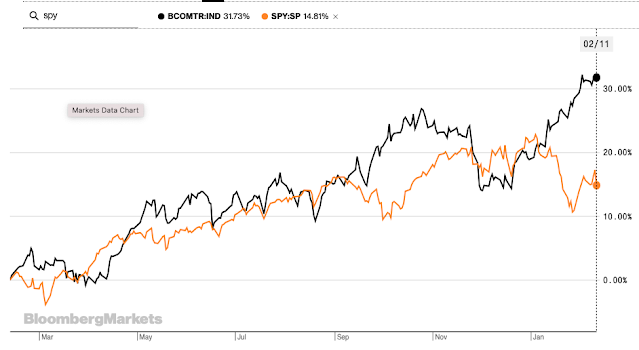

Some have taken this anti-bond view to an extreme, see "Endowments and equity factor - Just too much exposure?", yet there is still an inertia with many concerning fixed income. It has been a good hedge and many think it will continue to be a good hedge. The facts suggest otherwise as the stock/bond correlation has turned positive.

The problem is that investors cannot have everything with their fixed income. Real rates are negative and there is little near-term improvement. Inflation may revert from current highs, but without a significant increase in nominal yields, real yields especially for short maturities will be unattractive.

A combination of low yields, negative returns, and a positive correlation to stocks make alternatives much more attractive, but there still needs to be a focus on the switching of risks.

Hedge funds need to show positive real returns if they are to be an effective alternative. Right now, there is a five percent inflation hurdle for alternatives. This seems like an easy threshold to beat; however, alternatives still must deliver. If there needs to be a real return as compensation for risk, the nominal returns should be well north of the 5% level.

Fixed income Treasuries are usually a liquid investment. That assumption has been tested in March 2020, but generally it still holds. Moving to alternative investments will have a liquidity cost that needs compensation.

By most definitions, moving out of Treasuries or liquid bonds will require taken on more volatility and increase investor risk. Anything other than Treasuries will require taking credit risk.

There is a continued search for yield, but investors should not just look for close substitutes. The search for yield must include appropriate compensation for risk and liquidity.