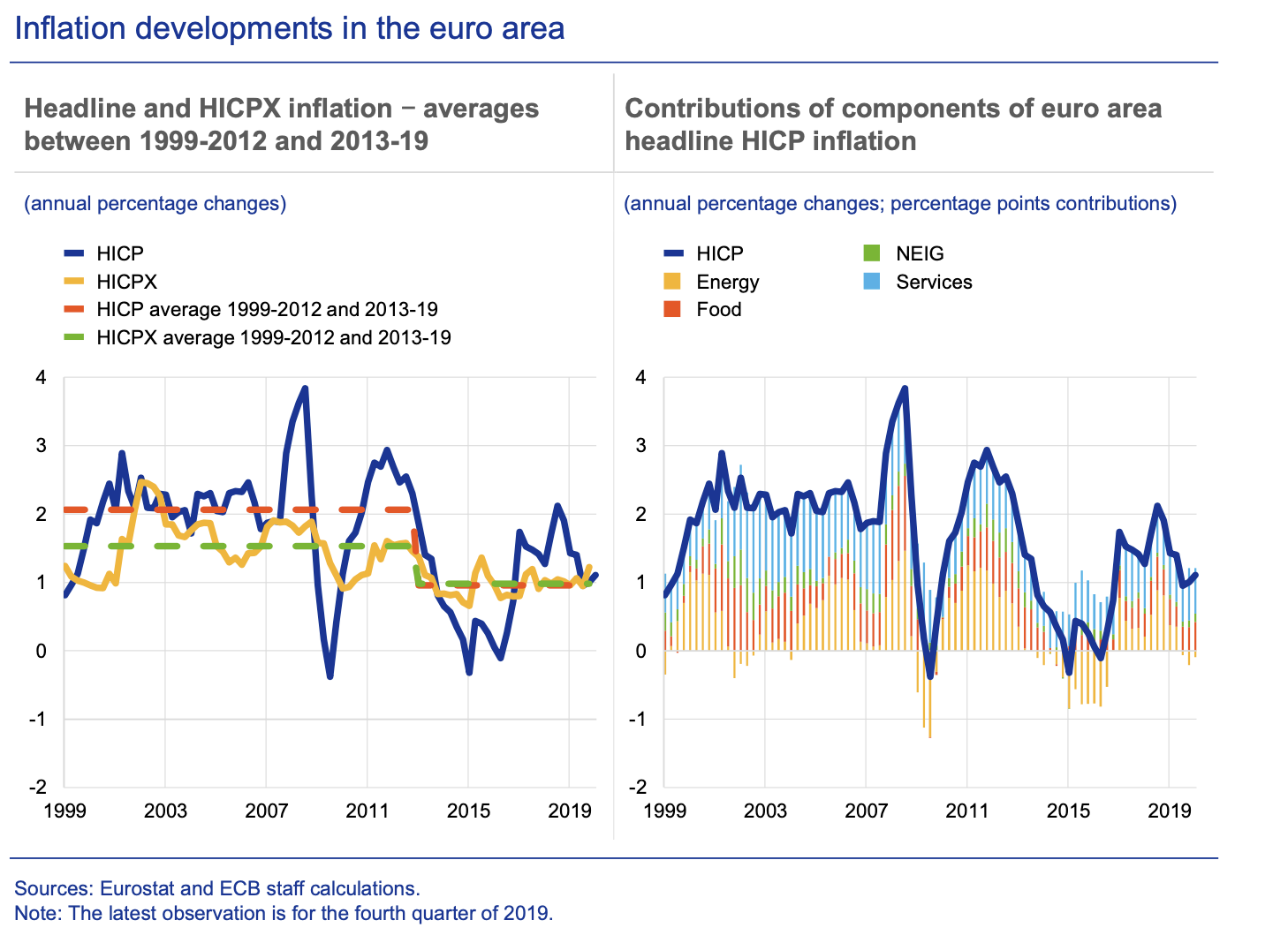

The ECB produced a deep study of Euro area inflation and why the central bank persistently got their forecast numbers wrong. (See "Understanding low inflation in the euro area from 2013 to 2019: Cyclical and structural drivers Occasional Paper series No 280.) It consistently over-predicted inflation for the 2013-2019 period. It is not clear that they will be better at forecasting in the future; however, this is an important piece of self-reflection and will be useful for other central banks. Overall, our ability to understand inflation drivers is poor and the implication is that policies will make inflation mistakes. Perhaps this decade will be a problem of under-predicting inflation.The reasons for the poor predictions are numerous; however, the key may have been an inability to properly measure economic slack. The Phillips curve is alive and well; albeit with a different slope and structural factors that are not included in the model. Currently, central banks have an inability to measure economic tightness. Of course, the lower bound problem is discussed but an inability to forecast inflation makes the bound problem moot.The slack problem is associated with structural trends like globalization, digitization, and demographics which provided strong headwinds against inflation. The twin crises over the last fifteen years also provided shocks that created persistent slack. The ECB also notes the disconnect between the bank's goals and inflation expectations, the anchoring problem. Put another way, the market's expectations were better grounded than the ECB's view.

No investor should be surprised by the poor forecasting of inflation by central banks. Poor forecasts leads to policy mistakes.

No comments:

Post a Comment