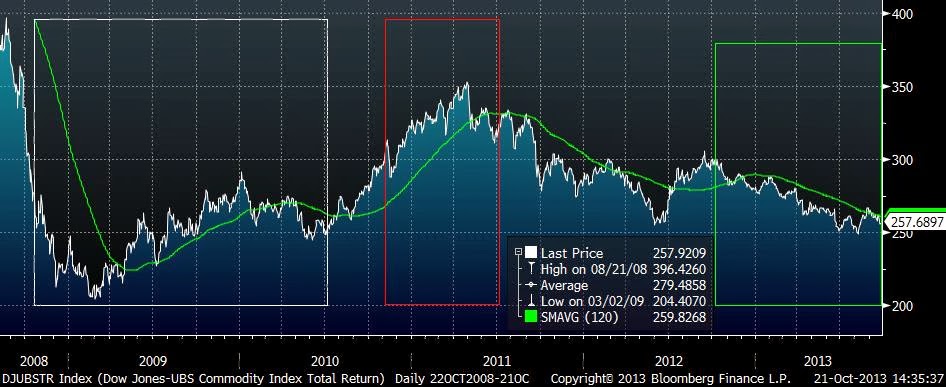

QE has not had the impact expected on commodity markets. Highlighting the three periods of quantitative easing suggests that more money has not increased commodity demand and ultimately prices. This is not what the central bank doctors have ordered. In fact, their efforts to increase global demand has not worked with the most recent easing.

QE1 provided the support necessary to stop the decline in commodities and the Great Recession. Prices bounced off the lows. With QE2, there was a another surge in commodity prices albeit the reaction was not as great and prices started to fall near the end of the easing period. By QE3 the addicted global economy needed a bigger fix to get prices moving and so fall there has not been any help. If the Fed wants higher commodity prices, it is going to have to do more purchases not less, or the Fed could conclude that the purchase program is just not working and move to some other strategy.

The apologists could say that things would be worse with less or no purchases, but it seems as though the markets needs something more than the current stable buying program to get demand to increase.

QE1 provided the support necessary to stop the decline in commodities and the Great Recession. Prices bounced off the lows. With QE2, there was a another surge in commodity prices albeit the reaction was not as great and prices started to fall near the end of the easing period. By QE3 the addicted global economy needed a bigger fix to get prices moving and so fall there has not been any help. If the Fed wants higher commodity prices, it is going to have to do more purchases not less, or the Fed could conclude that the purchase program is just not working and move to some other strategy.

The apologists could say that things would be worse with less or no purchases, but it seems as though the markets needs something more than the current stable buying program to get demand to increase.

No comments:

Post a Comment