Gold is now over $3000 an oz. and like any market that has a strong run-up in price there is talk of a bubble. The bubble talk becomes stronger when it is unclear what are the drivers for the increase in gold prices. The classic story is that gold rises as an inflation hedge, yet inflation has fall from its higher levels post-pandemic. We have seen the jump from $1250 pre-pandemic to the $2000 level at the end of 2023. Now we are seeing a move to $3000 which suggests that a new story is needed to explain the move.

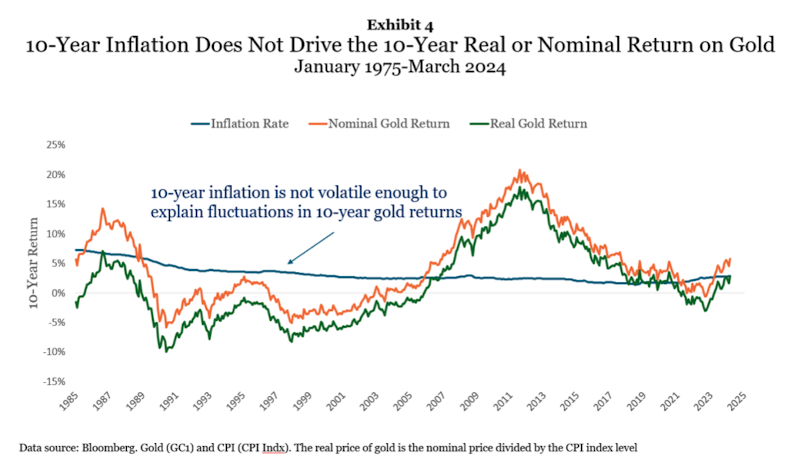

Erb and Harvey in their new paper "Is there still a golden dilemma?" offer a new view on gold which is both interesting and compelling. First, they show that inflation is not volatile enough to explain the variation in gold. Second, they find that there is a distinct change in the gold market based on the composition of buyers. The introduction of gold ETFs has made it easier to purchase a form of gold return which has increased the trend. Make it easier to purchase and demand will go up. Three, there has been an institutional change in gold demand based on de-dollarization. Given the dollar is being used as a form of financial statecraft to punish bad actors, there is a move by several countries to reduce their dollar holdings.

Erb and Harvey offer an explanation for the rising prices but there is a problem. This explanation just suggests that there are new buyers that are pushing the real price higher based on economic or political expectations. There is no central driving force that will suggest prices should be higher. Expectations dominate bubble thinking, so it is hard to know whether a higher real price is sustainable or will be reversed as in the past.

No comments:

Post a Comment