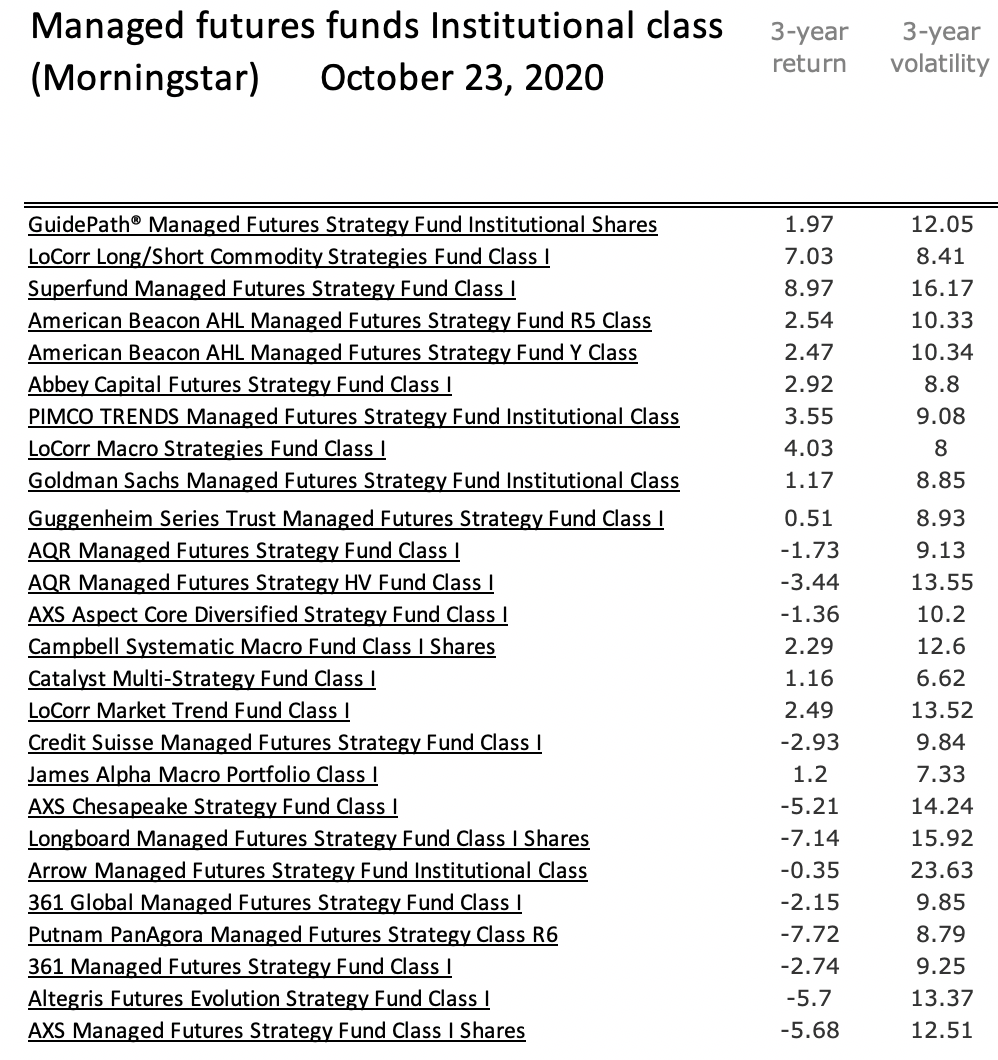

A frustration with any investment choices across asset management styles or risk factors is when the actual return to risk is negative. A basic premise for investing is that higher risk will be compensated with higher return. However, there is a big difference between "will be" versus "should be", a big difference between expected return versus actual return, and a big difference between risk/return trade-offs in the short-run versus long-run.

When the return to risk is negative over a term of say three years, investors will generally avoid the style, or at least be more cautious concerning any decision for risky managers. The chart presented for managed futures is not unique to this return to risk problem. It just happens to be a focus for my current attention. I charted the return to risk for managed futures funds institutional classes listed on Morningstar for the last three years. Higher volatility did not guarantee any positive return.

A contrarian may say this cannot last and choose the fund with the greatest return to risk versus longer-term averages, but a more conservative investor will just avoid the risky managers until there is some clear compensation for risk.

Of course, for a defensive situational investment, return to risk may not be relevant but a mistaken measure of investment success. Managed futures (mainly trend-following) is expected to do better during market divergences, yet there is no reason why any rolling three year period return to risk has relevance for choosing a strategy that thrives during focused periods of market dislocation. Investors will pay a price for convexity; nevertheless, they should still be compensated for buying a riskier managed futures style especially if there is a period of market divergence.

No comments:

Post a Comment