Commodities markets are not all the same and some of our assumptions concerning long-term real prices are wrong. Bundling all commodities together is wrong. Of course, for many investors these conclusions are obvious, but the historical price research by David Jacks of Simon Fraser University shows in great detail that over the long-run real prices for commodities can behave very differently. See his paper "From Boom to Bust: A Typology of Real Commodity Prices in the Long Run". Jacks does a good job of providing detailed information on real prices for 30 different commodities over 160 years. He provides a wealth of charts in his paper. His key conclusions should be remembered by any commodity investor.

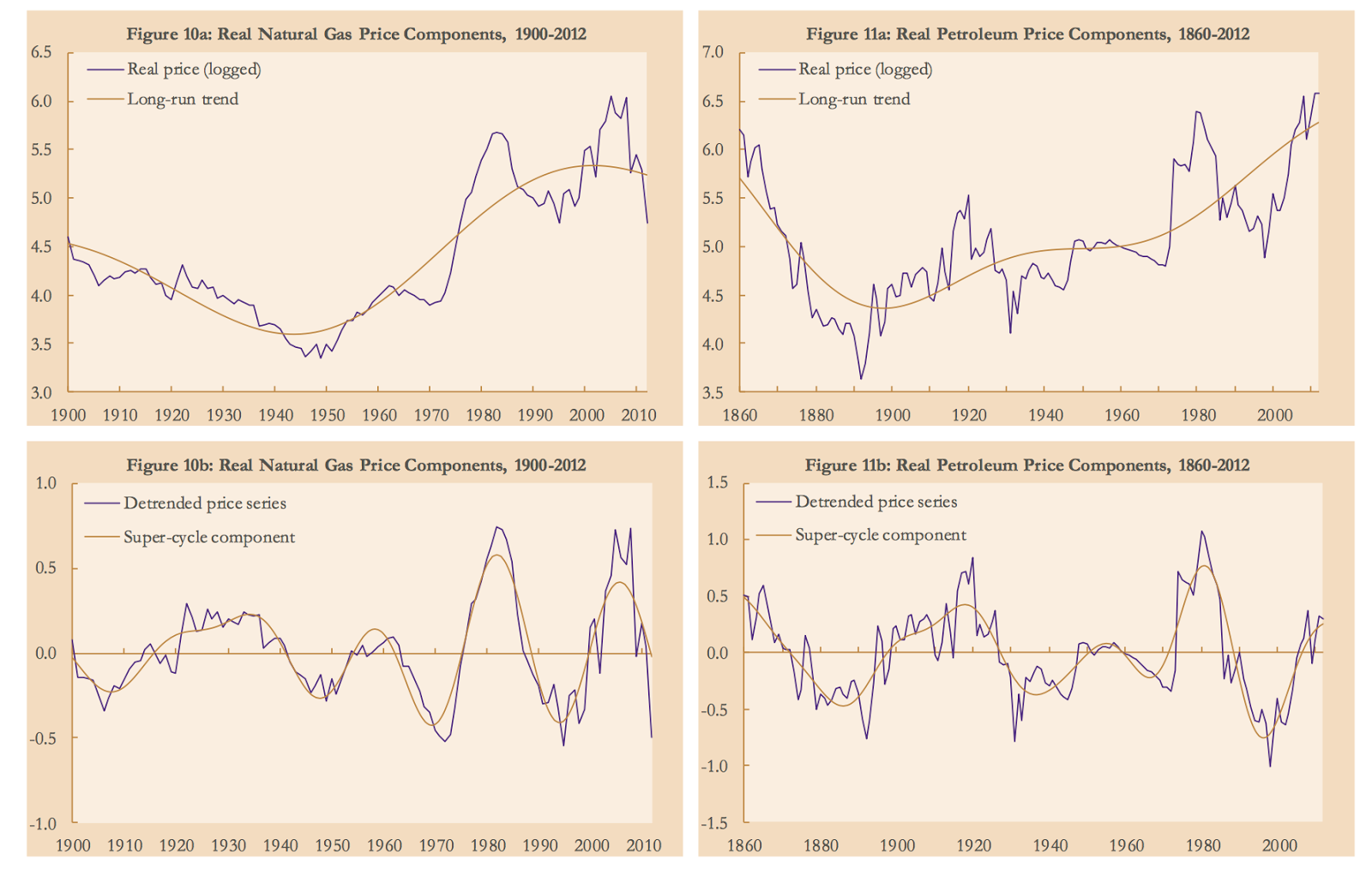

There are some simple broad views about long-run commodity prices. First, they can have long cycles. Call it super-cycles, but commodities can go through strong uptrends from a combination of supply shortages and increased demand only to reverse after production catches up with demand. These cycles can last well over a decade but will eventually be reversed. Second, the real prices of commodities have not all been declining. There is the adage that being long commodities means being short technology. The reality is more complex and cannot be applied to all markets. The more recent decades have shown an increase in real prices versus the earlier history presented. Third, periods of boom and busts occur with large swings in prices. These have not been dampened over the last few decades. In fact, the swings have been more extreme.

As important as the general price conclusions is the fact that all commodities cannot be classified the same. Nevertheless, we can break commodities into two major types, commodities to be grown and commodities in the ground. In general, we can conclude that commodities to be grown have shown secular real price declines. There have been technological advancements that have led to higher productivity in growing. You can think of the advancements in genetics, fertilizer, and mechanization to increase productivity as the drivers of the real price decline. For commodities in the ground, there is a different story. We may be able to better extract oil and minerals, but the supply is still finite. As the supply is used, there is a battle between better technology and the difficulty of extraction.

All commodities cannot be classified as the same and even in the short-run, the dynamics of growing versus extracting are important. Here is a sample of the charts developed in the paper.

There are some simple broad views about long-run commodity prices. First, they can have long cycles. Call it super-cycles, but commodities can go through strong uptrends from a combination of supply shortages and increased demand only to reverse after production catches up with demand. These cycles can last well over a decade but will eventually be reversed. Second, the real prices of commodities have not all been declining. There is the adage that being long commodities means being short technology. The reality is more complex and cannot be applied to all markets. The more recent decades have shown an increase in real prices versus the earlier history presented. Third, periods of boom and busts occur with large swings in prices. These have not been dampened over the last few decades. In fact, the swings have been more extreme.

As important as the general price conclusions is the fact that all commodities cannot be classified the same. Nevertheless, we can break commodities into two major types, commodities to be grown and commodities in the ground. In general, we can conclude that commodities to be grown have shown secular real price declines. There have been technological advancements that have led to higher productivity in growing. You can think of the advancements in genetics, fertilizer, and mechanization to increase productivity as the drivers of the real price decline. For commodities in the ground, there is a different story. We may be able to better extract oil and minerals, but the supply is still finite. As the supply is used, there is a battle between better technology and the difficulty of extraction.

All commodities cannot be classified as the same and even in the short-run, the dynamics of growing versus extracting are important. Here is a sample of the charts developed in the paper.

No comments:

Post a Comment