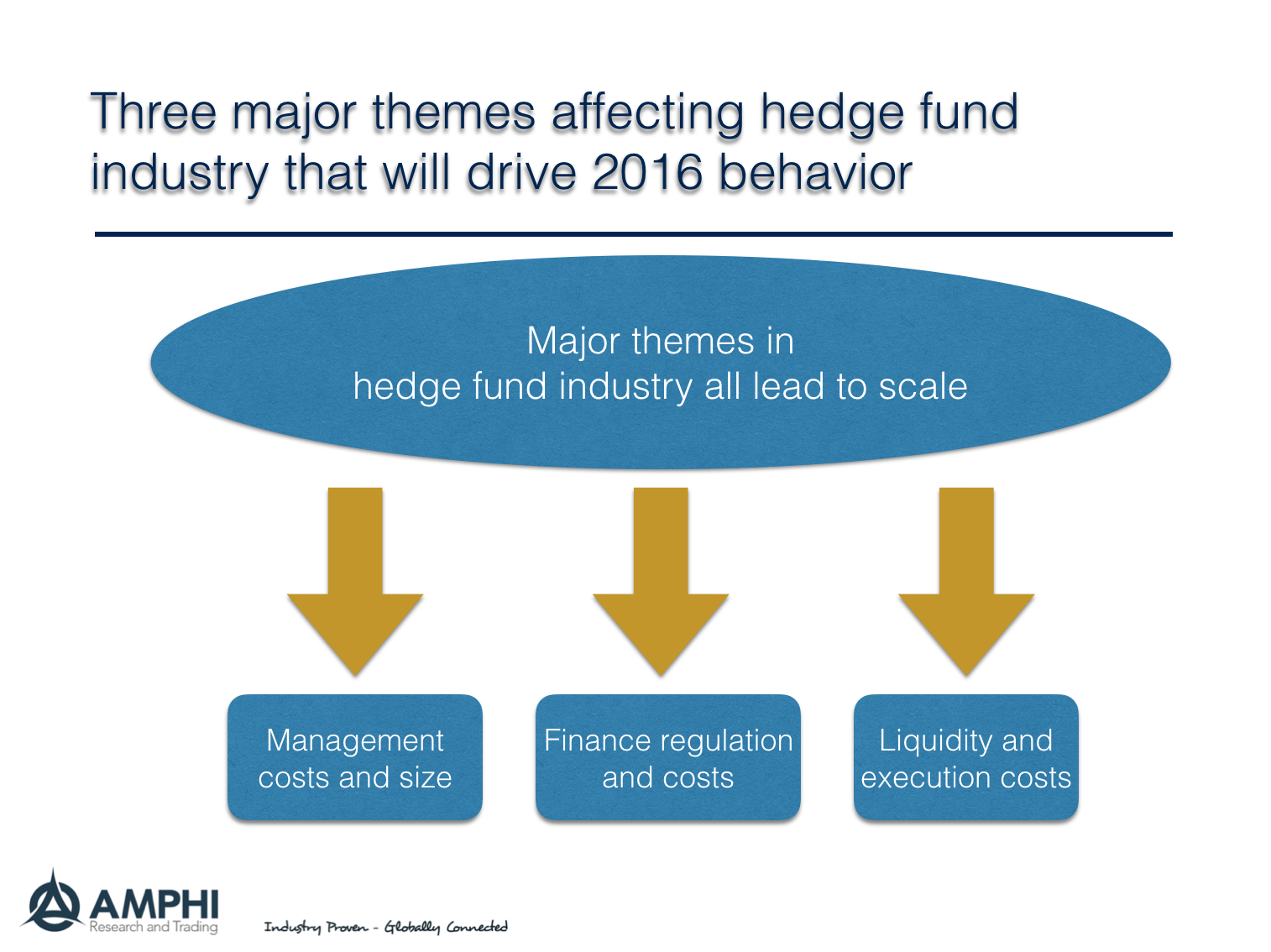

The economies of scale and money management

Management costs and size

Economies of scale become even more important when there is a down year with less manager return dispersion. When there is a down year for many hedge fund styles and managers like what we are likely to see in 2015, the power inherent in economies of scale become even more acute.

When performance is down, there will no incentive fees to lean on to help pay the bills. This issue is especially the case for smaller managers. Small firms cannot use the incentive fees to recoup their start-up costs and management fees are just too low. Down years also lead to more manager switching, so marginally sized managers who lose assets will be harmed more. If there is little dispersion in returns, investors will use other criteria for determining investment decisions. Size will matter more in these cases. What you gain with economies of scale in up years, you lose in down years. Fixed costs are harder to cover.

The industry has seen some large fund closings especially in global macro. While these firms were big, they were not able to generate the internal returns necessary to pay talent, generate future returns, and cover all costs. If alpha is harder to identify, there needs to be more talent at work which increases the fixed cost of doing business. To gain scale managers are offering more products which actually may dilute the talent pool.

If there is more fee compression, larger firms will be better able to either sustain a fee cut. Surprisingly, larger firms have been able to maintain fees better than small firms which is another scale problem. With the retailization of funds, scale is also more important in order to have the marketing to reach smaller investors.

Expect more firm closings and greater average size for managers. Talent in small firms will be harder to find.

Regulation and money management

It is generally found that more regulation places greater cost on small firms than large firms. Hence, there is a greater pull for scale because legal and compliance staffs are a necessary fixed cost. We are not arguing about the efficacy of any regulation, but it has clear impact on the cost of doing business. Firm failure, fraud, and financial contagion also have high cost, but it is not clear how the costs benefit analysis has been done.

The regulation of banks and other financial institutions leads to carry-over effects on all money management firms. Prime brokerage and clearing becomes more expensive. Bank have to hit higher capital requirements and ROE targets in the current environment. This also drives the industry to seek scale.

Consolidation because of clearing and regulator costs will affect all hedge funds and lead to firm consolidation.

Liquidity and execution behavior

There has been more discussion on liquidity in different markets. We have seen flash crashes in all of the major asset classes, equities, fixed income, and currencies. The money management and hedge fund industry have taken note of the potential problem. We have seen special round tables within the CFA to discussion corporate fixed income liquidity. The Fed has focused research to determine whether there is a liquidity proble in key markets. There answer is no. All this means is that trading and liquidity decisions will be more important in 2016. There will be more effort to improve the execution process but this actually may be at odds with trends in regulation.

At the same time, the open outcry trading floors have closed in Chicago and there has been more government scrutiny and prosecution of HFT traders and dealer manipulation. Algo trading is still growing but there is a new air of caution conquering what can be done to send and pull orders from the markets.

More money will be spend on better execution. This has the potential to improve returns, but it creates another barrier to entry for the small firm that does not have access to technology.

Conclusion

Get bigger or you will be crushed under scale, regulation, and execution costs.