1. yield

2. duration or the potential for rate declines

Neither look good for the longer-run.

Yields are not going to help with fixed income this year. First, the level of yields is low. Hence, there is less cushion associated with any fixed income security. The duration of any bond for a given maturity has lengthened given the lower coupons. Second, the yields are below current inflation rates for many maturities. There is no real return and any movement back to a real positive yield will mean higher absolute yields which will be bad for total return. If rates, however, stay the same with current inflation, investors are getting a raw deal.

The duration effect for total return is based on the ability of yields to fall. There is less room for rates to fall hence duration gain will be limited and one-sided. Clearly, the increase in rates over the last six months have made new trades better but there is still limited gains with 10-year yields just below 2% and 30-year at just over 3%.

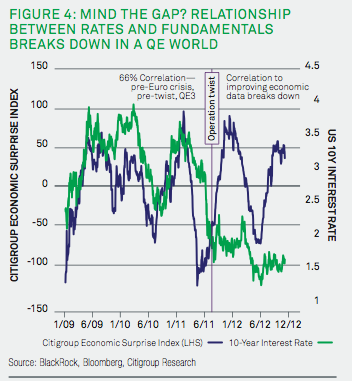

The environment is poor given financial repression. This interesting chart from Blackrock shows there is less connection between fundamentals and rates.

The search for yield and return has matched the expansion of money but the recent talk about exit strategies can easily spook the market.